Startup founders are among the most important people in our society: their ambition and creativity drive innovation, solve hard problems, and disrupt lazy incumbents by building something from nothing. Unsurprisingly, they have become the rock stars of our age and the embodiment of the American Dream. However, with a 90% failure rate, guaranteed loss of friends, and little to no sleep, the life of a startup founder is a lot less glamorous than success stories on TechCrunch would have you believe.

It is always important to remember that billions of dollars from highly publicized IPOs do not land directly in founders’ pockets — and, conversely, that many founders whose companies do not reach the coveted “unicorn” status can still be successful, reap considerable financial rewards, and make a meaningful contribution to their industry and society. In both cases, the founders’ control over the company and its equity can determine the outcomes for everyone involved.

As the company grows, hires, and receives external funding, founders’ equity will inevitably become diluted. The intricacies of vesting schedules and liquidation processes complicate the matter even further. This may seem daunting at first, but it is a normal and necessary part of building a successful company. To maximize their returns, founders must start off with a clear understanding of how their share of equity will change over time, plan ahead, and account for multiple courses of action.

There are multiple factors that will impact a founder’s ownership in their business:

- Equity distribution among multiple founders

- Employee stock ownership

- Priced rounds

- Re-vesting schedules

- SAFE and convertible notes funding

- Founder ownership augmentation

- Liquidity strategies

I break down each factor below.

Impact of Multiple Founders on Equity

The first big decision comes on day one: dividing equity among founders.

An even split is the simplest, but there are often other considerations. Originators of the idea, founders who take on leadership positions, and those who take on a higher degree of risk rightfully command a greater share.

When you are starting a business with people you like and trust, the decision on the initial equity distribution might feel natural and intuitive. It is hard to imagine future disagreements, but circumstances (and people) change. This is why the founders’ agreement should outline the equity split, roles, responsibilities, and vesting schedule. Discuss all these details beforehand and be mindful of assumptions: writing everything down in a legal document prevents future disputes and goes a long way to keeping the business stable.

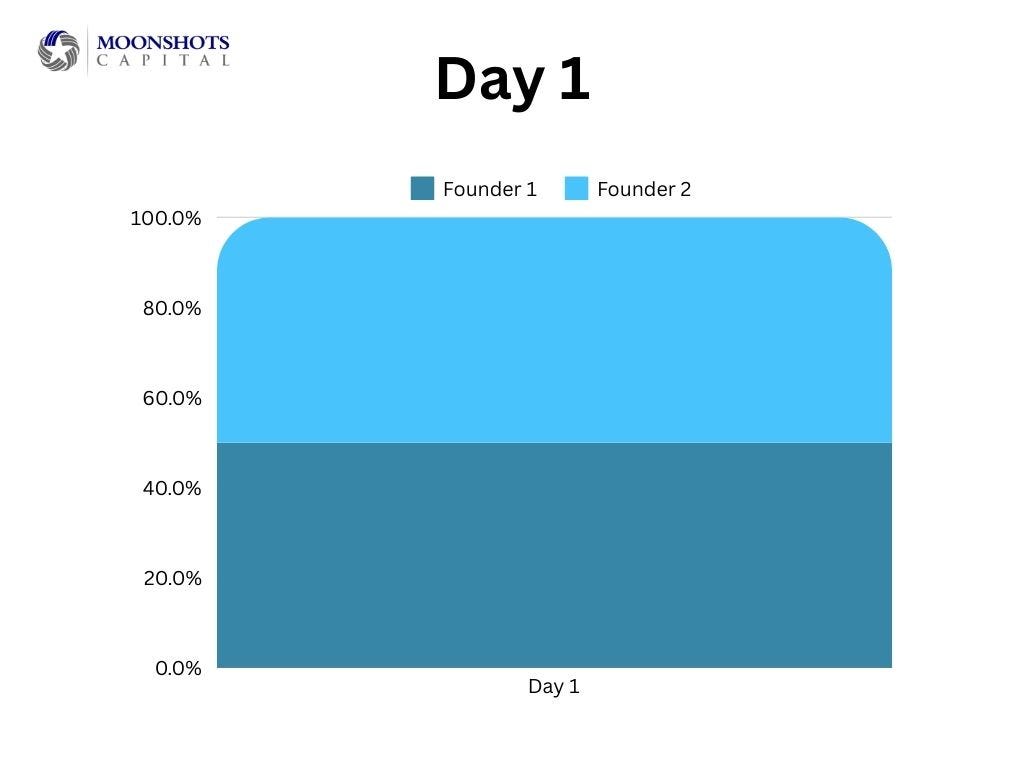

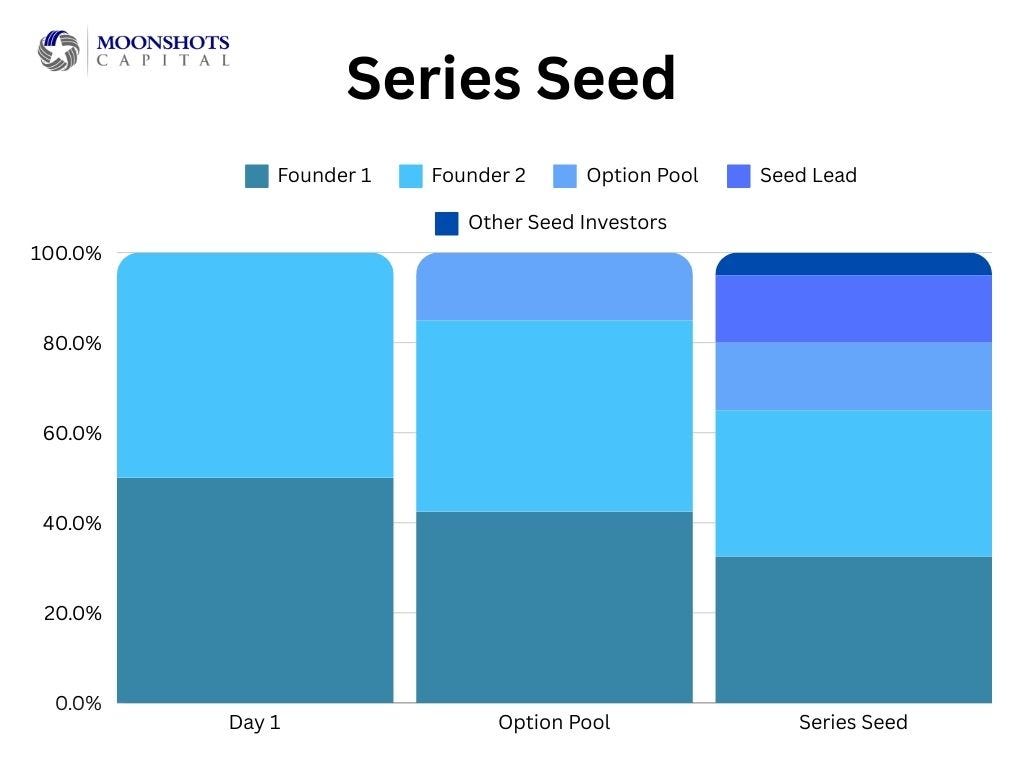

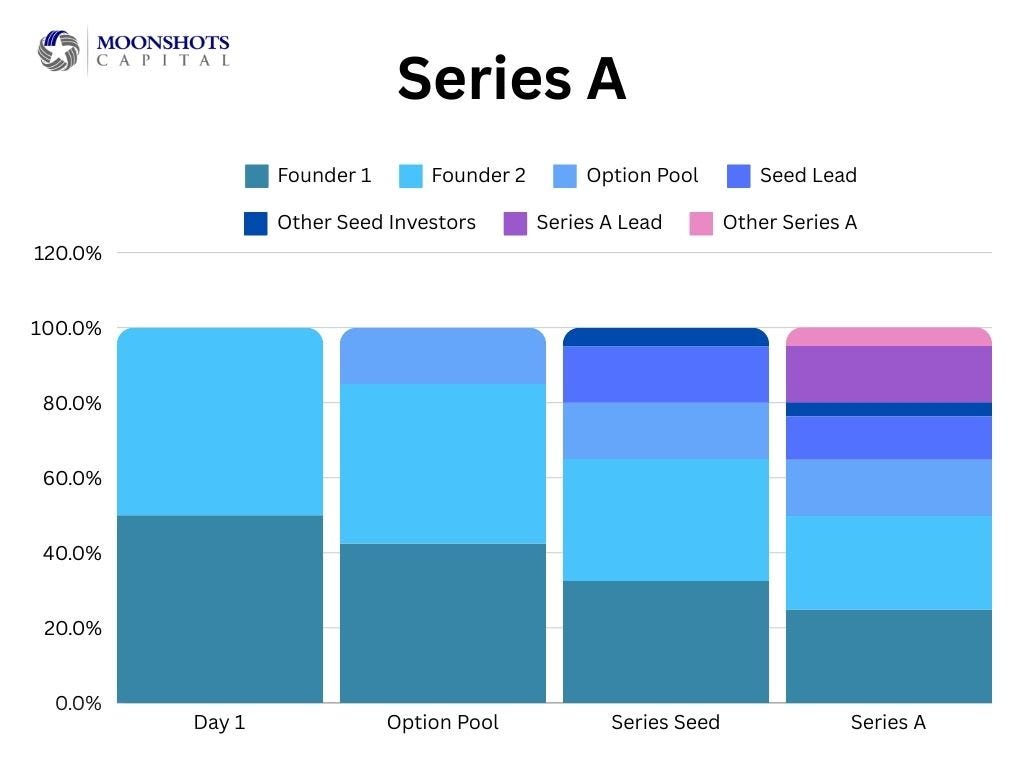

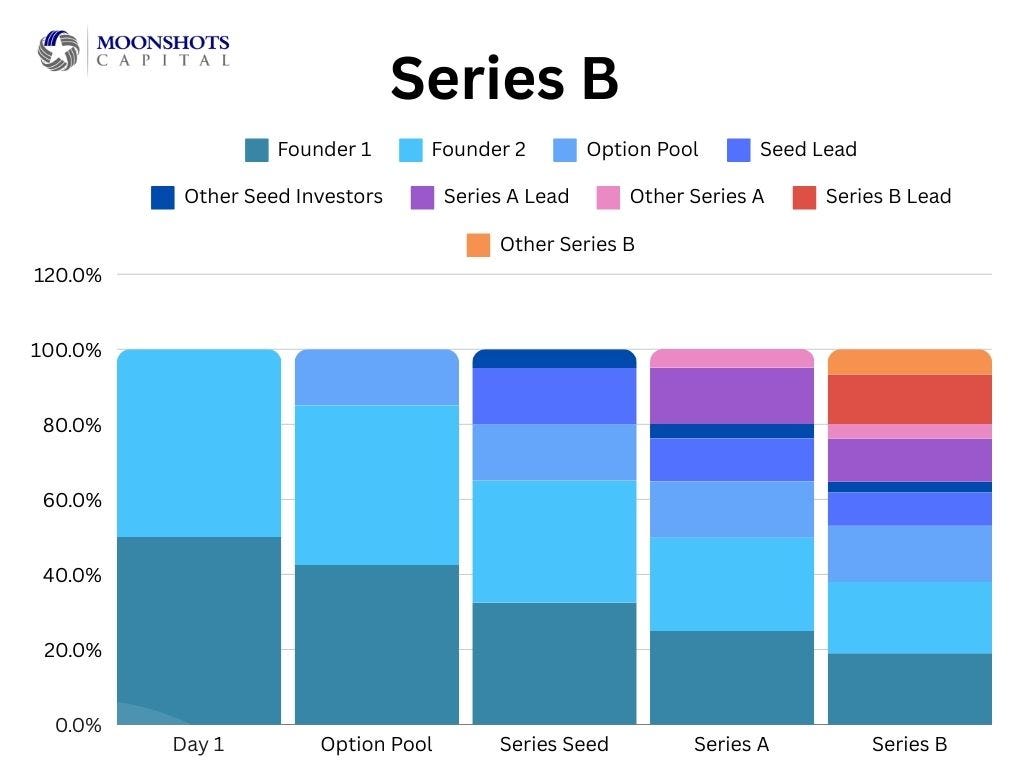

To start, let us imagine a dream team of two founders: a CEO and a CTO, splitting all the work evenly and doing it all alone in the company’s early days. Their cap table looks very clean:

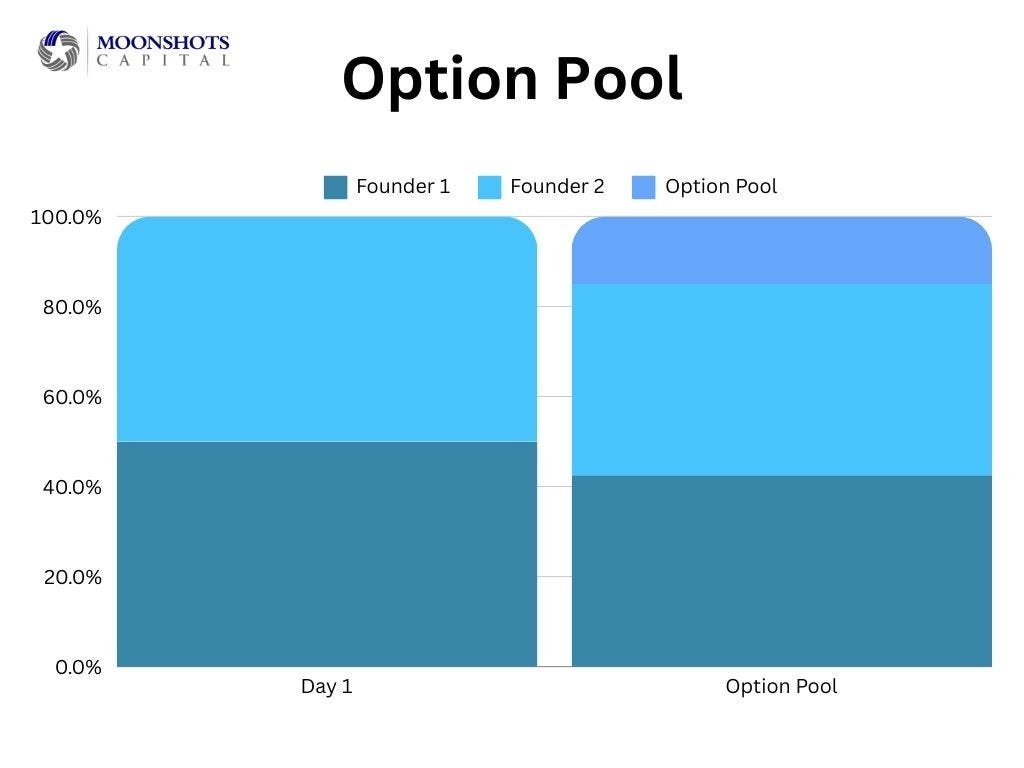

However, our “dream team” will not be able shoulder everything alone indefinitely. Soon, they will need to hire, and they are unlikely to be able to offer impressive wages when they are just starting out and have little cash.

Employee Stock Ownership (ESOP) in a Startup

To recruit and motivate top talent, most startups will put in place an Employee Stock Ownership Plan (ESOP), which provides a company’s workforce with an ownership interest in the company as part of their compensation. Businesses usually set aside 10–20% for the ESOP — let us say our two founders decided on 15%. And just like that, their respective shares of equity dropped from 50% to 42.5% each.

Employee stock ownership is not “lost forever.” Just like the founders’ equity, employee stock depends on a vesting schedule, which dictates how long employees must stay with the company before they fully own their share.

An employee or founder may leave before they meet all the conditions of their vesting schedule. They may also prefer liquidity to equity and offer the company an opportunity to repurchase their stock instead. In those circumstances, some equity goes back to the remaining stakeholders. On the other hand, the company may need to introduce more equity into their employee option pool as the company grows. Typically, each major round of financing requires a “plus up” of the ESOP to 10–15% at a minimum. To keep our example simple, we will assume that these fluctuations even out over time.

Understanding Priced Rounds

Congrats! You are gaining traction, and venture capital investors are showing interest in supporting you. You need that money to grow — but each priced round will result in more equity dilution. Depending on your strength at the negotiating table, you will typically have to let go of as little as 10% and as much as 30%. Let us assume the lead investor in a Series Seed gets 15% of our example startup’s equity, and other investors jointly get 5%. The equity share of each founder now drops to 32.2%.

Hopefully, your startup will continue growing and attracting new investors. That means that the founders’ equity share drops once again. At the end of a Series A financing with 20% dilution from investment and 5% from an increase in the ESOP (total of 25% dilution), each founder will own 24.9%.

At the end of Series B funding round with another 25% dilution, each founder’s equity ownership will drop to 19%.

If you can grow your business further — possibly to a multi–billion–dollar valuation — you will likely need more capital for organic growth or acquisition. To do that, you will raise more funding, incurring additional equity dilution. However, the pie is ostensibly getting much bigger, so your smaller ownership percentage is actually worth a lot more absolute dollars.

Re-vesting Equity

Priced funding rounds frequently have another effect on equity. New investors will typically require re-vesting by the founders that are in key roles — that is, adjusting the vesting schedule for founders (and potentially some key employees) to ensure long-term commitment. Effectively, the investor wants assurances that if you leave the company, the company will retain enough of your unvested equity to use for compensating your replacement.

The extent of re-vesting depends heavily on the stage of the startup and the performance of the company and its leadership, including new executive hires. Re-vesting may mean restarting the vesting period entirely — although this is not typical — or simply modifying the outstanding terms — say, re-vesting 50% or 75% of equity over a four-year period. Sometimes, only a portion of unvested shares is subject to re-vesting, while the already vested shares remain unaffected. This does not immediately change overall equity ownership percentages, but it may impact the amount of money the founder will eventually be able to realize at an exit.

Re-vesting negotiations require keen self-awareness, situational awareness, and sound judgment. As a founder, are you truly prepared to commit to more years actively running your startup? Is the new schedule fair to the employees who worked hard to get closer to full ownership, or will it yield disgruntled resignations instead of retention? Come to the negotiating table with clear answers to these questions in your mind, and you will have a much better chance of walking away with the best deal possible.

Bridge rounds: SAFEs and Convertible Notes

SAFEs and convertible notes allow investors to provide capital to startups up front and get equity down the line during a subsequent financing round. You will not see the impact of that deal on your cap table right away but make no mistake: they are just as dilutive as a priced round — the math just gets calculated at a future date.

Investors providing SAFE and convertible note funding are not entitled to any specific percentage of your equity. Instead, they will ask for a certain number of shares. Since you do not know what the price per share will be in your next round, you will typically set a cap on the maximum valuation at which they will convert. Some SAFEs will also include a discount rate of 10–20% that allows existing investors to obtain shares at a lower price than new investors. Very importantly, SAFE financing does not have a repayment obligation. This means that the founder will not be “on the hook” for the money if the startup goes under. The investor will not be repaid, and there is no collateral.

Convertible notes, on the other hand, are a form of debt that does need to be repaid — often with interest. Convertible notes are also frequently collateralized by the startup’s assets or intellectual property. Convertible notes have a maturity date by which they need to be converted into equity, repaid, or renegotiated. When a note matures, investors will collect equity at a pre-agreed valuation cap or discount rate even if there has not been a new financing round. Alternatively, they may demand repayment of the principal plus accrued interest — and they can enforce that through legal means. Some difficult fundraising markets can result in more unfavorable terms on convertible notes, such as liquidation preferences where the investor can get some multiple of their investment in the convertible note before anyone else in the equity stack participates. Terms like these can result in even greater dilution if things do not go well.

In both cases, it is impossible to predict with 100% accuracy what proportion of equity your investors will own, but you can (and should) make reasonable estimates based on the trajectory of your startup and try to account for the most likely scenarios.

Founder Ownership Augmentation

Equity dilution is an inevitable part of growing a business, but after five or more years founders may find themselves wondering if there will be anything left for them at the end of the day. Fortunately, there are two scenarios that allow the founder to get some of the equity back.

If the founder remains with the company throughout its entire life cycle s, it may make sense to compensate for the dilution by granting them stock options from the ESOP on the same terms as regular employees — typically, four years of vesting with a one-year cliff.

Founder Equity Tax Treatment

Some equity may qualify for very favorable tax treatment for Qualified Small Business Stock (QSBS). You need to meet certain requirements to be eligible, including your company type, amount of gross assets, how much of the assets are used in your business, how you obtained your stock, and how long you have held it. Depending on your status regarding these criteria, you may be able to exclude a significant portion of capital gains generated from the sale of QSBS from your federal income tax bill — and sometimes your state tax bill as well.

However, if you are not careful throughout the process and do not understand your overall situation well when making filing decisions, tax provisions that seem beneficial initially may also work against you. Throughout your company’s life span, make sure you are always armed with an experienced tax professional whenever you are making decisions about changes to your cap table. Detailed record-keeping is crucial: whenever you claim a tax benefit, you need to make sure you have all the supporting documentation at hand to prove eligibility.

Liquidity

Eventually, there will be several ways to cash out equity under different conditions.

Exiting Your Startup through Mergers and Acquisitions (M&A)

If your startup merges with or gets acquired by another company, you are most likely to receive immediate liquidity for at least some portion of your shares.

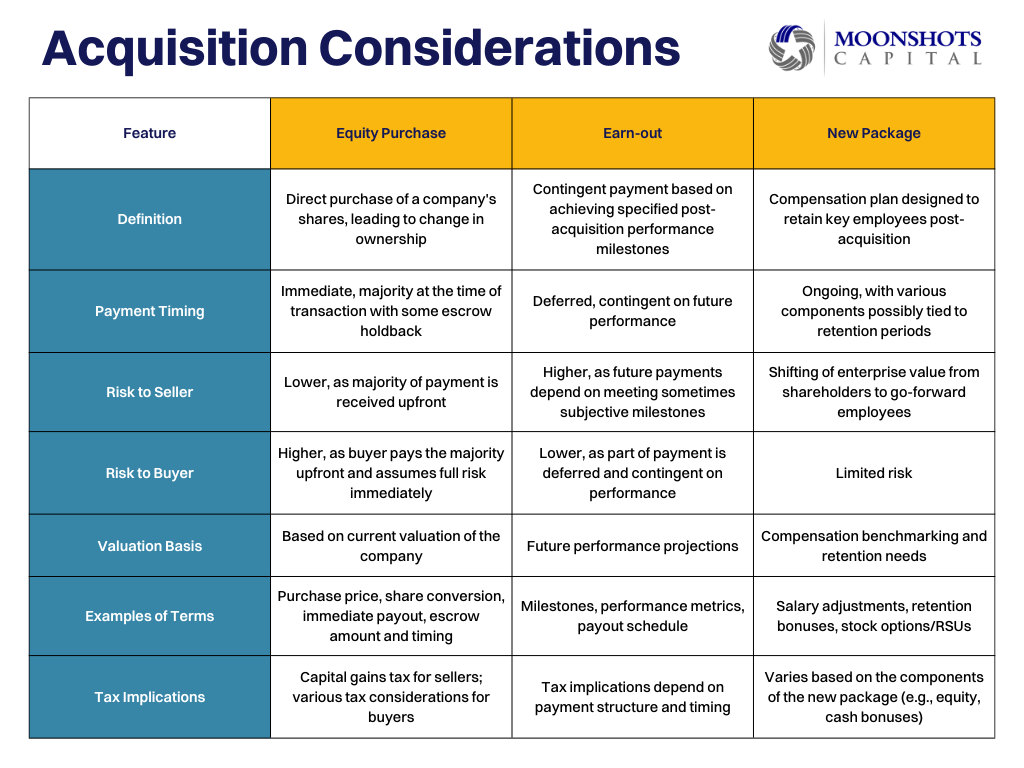

Typically, an acquisition comes with strings attached. An “earn-out” deal structure means that part of the purchase price will depend on your company achieving certain financial or operational milestones post-acquisition. In these circumstances, startup founders will stay with the acquiring company to ensure these targets are met. As with re-vesting, you should exercise excellent self-awareness and have a very good understanding of your company’s situation and how the integration will occur. Negotiate realistic targets, ensure you have the authority in the organization to execute on them, and do some self-reflection to confirm that you want to invest the necessary time and effort to continue working under the umbrella of a larger corporation.

If the acquirer wants you to stay, you can expect a new compensation package that includes a salary, a retention bonus, various perks, and frequently — equity in the acquirer. Here is a quick breakdown of possible M&A scenarios and their implications:

Secondary Sale

At certain points of a company’s life cycle, founders will have the option to sell some of their equity to new or existing investors without issuing new shares or waiting for an M&A or an IPO. The price of these shares is usually based on the company’s latest valuation but can also be negotiated as the purchasers will often request a discount.

Getting cash quickly may seem tempting at first, but secondary sales are more complex than they seem, and you should never make that decision lightly.

Most importantly, selling a significant portion of your startup shares impacts your voting rights and the degree of control you have over the company, especially as new investors may request a board seat. A large secondary sale by the founder may also impact employee confidence and morale. If the founder is looking to cash out quickly, does the company really have a healthy future? Existing stakeholders may also ask similar questions, and future fundraising efforts may be negatively affected as well.

Some key questions to ask are do you really need the money, do you really need that much money, and do you really need it now. Selling too much equity early might limit future gains if the company grows significantly. If the company is performing well, the market looks good, and a liquidity event is not too far off, you are likely to leave money on the table by letting go of your equity too early. Any secondary sale must be aligned with your long-term strategy and the company’s growth trajectory.

If you do decide that a secondary sale is right for you, you need to review existing shareholder agreements, which may include restrictions on share transfer, rights of first refusal by the company or other investors, and co-sale agreements. Your sale must comply with securities regulations and other legal requirements and, as always, you must evaluate the tax implications with experienced legal and tax professionals.

Initial Public Offering (IPO)

The IPO ends up being the path for some of the most successful companies. A company’s equity becomes available to trade on the public stock market. Founders will typically not be able to liquidate their stock immediately: there is usually a 180-day lock-up period after the IPO during which insiders cannot flood the market with shares and drive the price down. There are some special considerations for founders who begin to trade their own company’s stock: notably, they need to comply with SEC regulations about insider trading and ensure that rapid sale of a large amount of equity does not shake investor confidence.

Bottom Line

As you can see, there are many factors that impact the final equity ownership position of a founder. I urge all early entrepreneurs to map out the most likely courses of action they will follow to understand the ramification and conduct some sensitivity analysis.

At the end of the day, founders do suffer dilution in many ways; however, dilution also serves to grow the size of prize. It is much, much better to own 10% of a billion-dollar company than 100% of a $10 million business.

Moonshots Capital is a military veteran-founded venture capital firm that invests in early-stage startups with extraordinary leaders.

Subscribe to our newsletter for monthly updates about new investments, portfolio milestones, opportunities, and market commentary.

You can also follow Moonshots Capital and its General Partners on social media:

Moonshots Capital Twitter, LinkedIn

Kelly Perdew Twitter, LinkedIn

Craig Cummings Twitter, LinkedIn

Founder Equity Dilution in a Startup: A Walk Through the Process was originally published in Leadership Prevails on Medium, where people are continuing the conversation by highlighting and responding to this story.